Trusts, Companies, Super, Property and Personal Ownership Explained

High-income professionals often assume that earning more money automatically leads to building more wealth.

But after working with executives, doctors, lawyers, business owners and senior professionals, one pattern appears repeatedly:

Many high earners make great income – but structure their finances poorly.

The result can include:

- Paying significantly more tax than necessary

- Holding assets in the wrong entities

- Reduced borrowing capacity

- Increased legal risk

- Slower long-term wealth creation

Wealth isn’t just about how much you earn. It’s about how your assets are structured.

In this blog post, we’ll break down how high-income professionals should structure their wealth, including:

- Personal ownership

- Family trusts

- Companies and bucket companies

- Superannuation and SMSFs

- Property ownership structures

Understanding how these work together can dramatically improve tax efficiency, asset protection and long-term wealth outcomes.

Why Wealth Structure Matters

Before diving into structures, it’s important to understand why structure matters so much for high-income earners.

Australia has a progressive tax system, meaning higher income leads to significantly higher tax rates.

High-income professionals often face:

- Top marginal tax rates of 45% + Medicare levy

- Higher litigation and professional risk exposure

- Complex lending and borrowing considerations

- Reduced flexibility if assets are structured incorrectly

Without the right structure, you may end up:

- Holding investments in high-tax environments

- Exposing assets to legal claims

- Missing out on tax planning opportunities

- Restricting your ability to borrow and invest further

Strategic structuring helps achieve four key objectives:

- Tax efficiency

- Asset protection

- Flexibility

- Borrowing capacity

The most successful wealth strategies treat structure as a coordinated system, rather than a collection of unrelated investments.

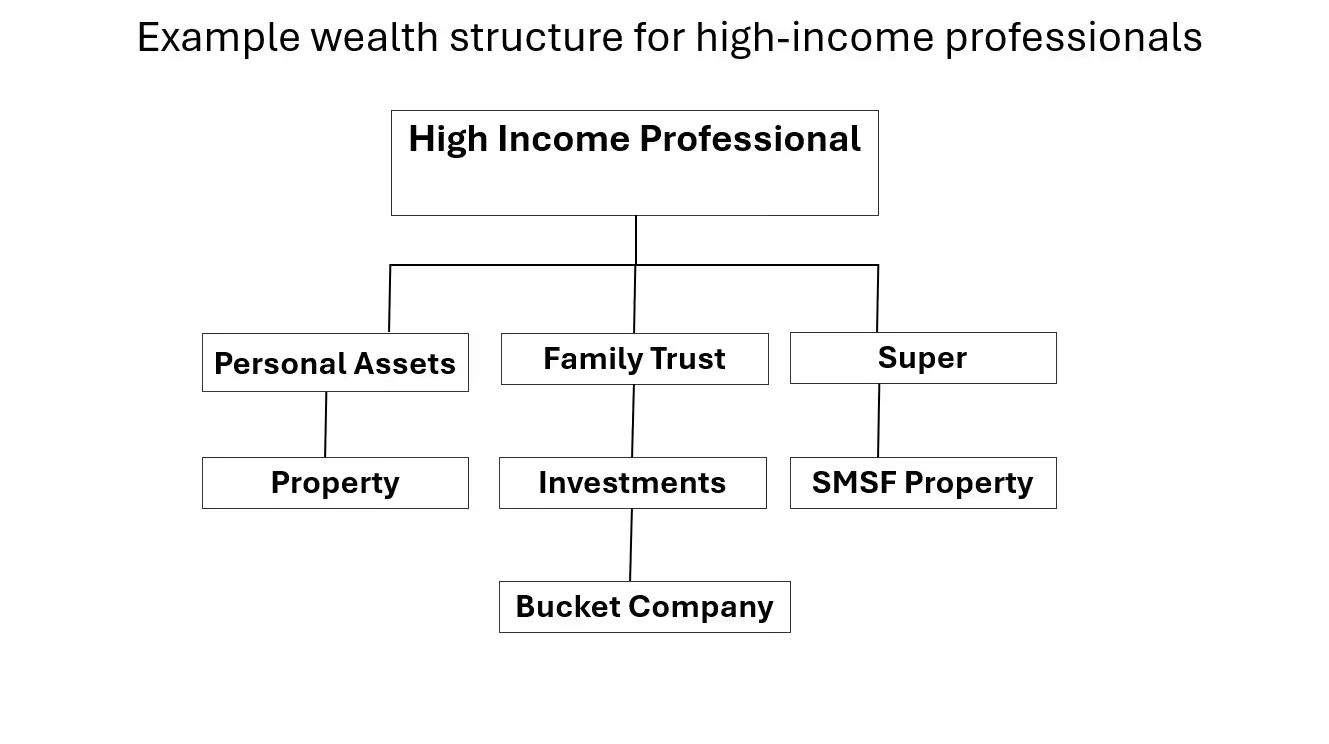

The Five Core Wealth Structures

For most high-income professionals, wealth is typically structured across five main ownership types:

- Personal ownership

- Family trusts

- Companies

- Superannuation structures

- Property investment entities

Each structure has different tax rules, lending treatment and asset protection characteristics.

Understanding when to use each one is key.

1. Personal Ownership

Personal ownership means holding assets in your own name.

This is the simplest and most common structure, and in some situations it is the most practical.

Advantages

Personal ownership works well when:

- Simplicity is important

- Borrowing capacity needs to be maximised

- Negative gearing benefits are required

- Access to capital gains tax discounts is important

For example, many professionals hold residential investment property personally because:

- Rental losses can offset personal income

- The 50% capital gains tax discount applies after holding the asset for more than 12 months

- Lenders generally assess personal borrowers more favourably than complex structures

Disadvantages

However, personal ownership has limitations.

High tax exposure

Investment income is taxed at your personal marginal tax rate, which for high-income earners can be:

- Up to 47% including Medicare levy

Asset protection risk

Assets held personally may be exposed to:

- Professional liability

- Litigation

- Relationship breakdowns

For professionals such as surgeons, directors or developers, this risk can be significant.

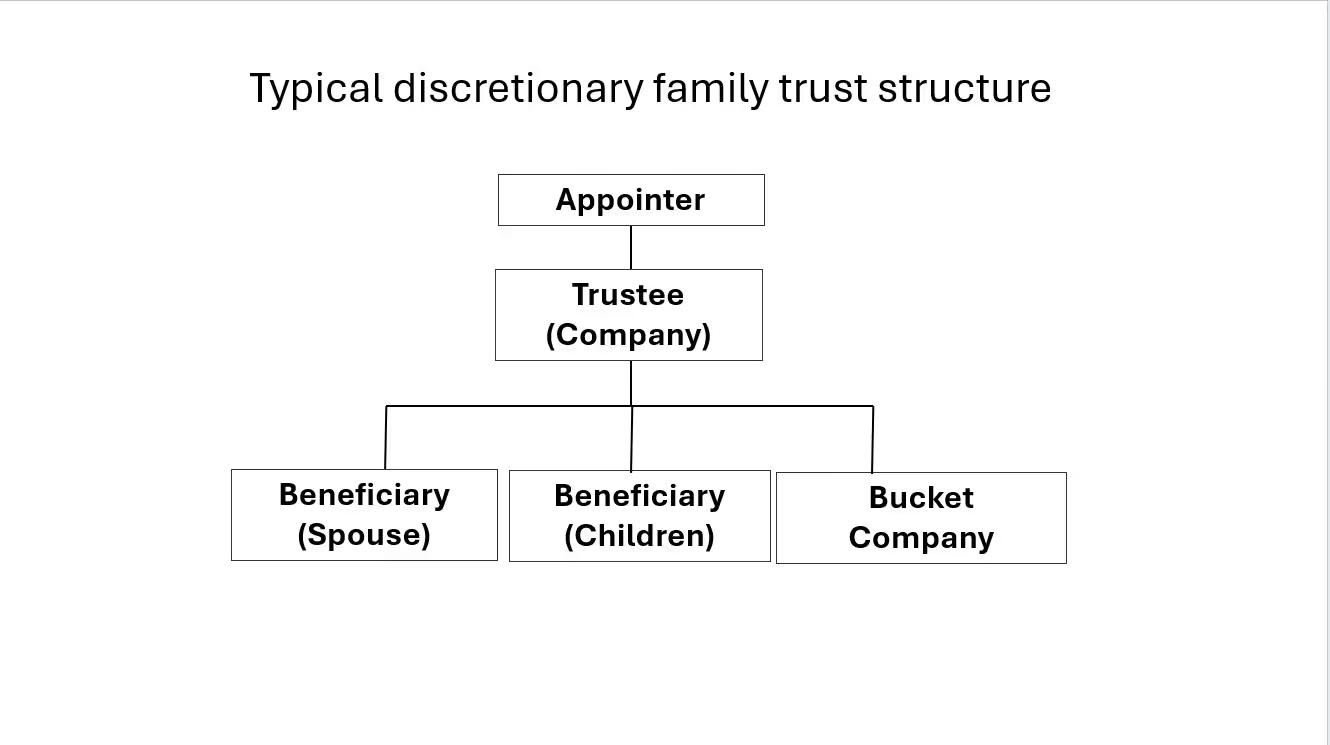

2. Family Trusts (Discretionary Trusts)

Family trusts are one of the most common wealth structures used by affluent families in Australia.

They provide flexibility, tax planning opportunities and asset protection benefits.

How a Family Trust Works

A typical discretionary trust involves several key roles:

- Trustee – controls the trust (often a company)

-

Beneficiaries – people who can receive income

-

Appointor – ultimate controller of the trust

The trustee distributes income to beneficiaries each year.

This allows income to be allocated in the most tax-efficient way.

Benefits of Family Trusts

Income distribution flexibility

Income can be distributed to beneficiaries on lower tax rates.

Example:

Instead of one person paying tax at 47%, income can be distributed across multiple family members.

Asset protection

Assets held in a properly structured trust may have greater protection from personal liabilities.

This is particularly useful for professionals exposed to legal risk.

Estate planning flexibility

Trust assets do not automatically form part of your personal estate, allowing more strategic succession planning.

Limitations of Family Trusts

Despite their benefits, trusts also come with some limitations.

Lending considerations

Some lenders treat trust borrowing differently, which can affect:

- Borrowing capacity

- Loan assessment

- Lending policy restrictions

However, many lenders do lend to trusts with individual guarantees.

Land tax considerations

In many Australian states, family trusts may have:

- Lower land tax thresholds

- Higher land tax rates

This can increase the long-term holding costs of property investments.

3. Companies and Bucket Companies

Companies are often used alongside family trusts to improve tax efficiency.

One of the most common strategies used by high-income families is the bucket company structure.

What Is a Bucket Company?

A bucket company is a company used as a beneficiary of a family trust.

If trust income is high, the trustee can distribute some income to the company.

Instead of being taxed at personal marginal rates, that income may be taxed at the corporate tax rate.

Typical company tax rates include:

- 25% for base rate entities

- 30% for larger companies

Why This Strategy Is Used

For high-income professionals paying tax at 47%, distributing some income to a company taxed at 25% can create a tax deferral opportunity.

The retained profits can then be:

- Reinvested

- Used for future investments

- Business opportunities

- Distributed later with franking credits

Important Considerations

This strategy must be implemented carefully due to:

- Division 7A loan rules

- Compliance obligations

- Tax planning considerations

Professional advice is essential when using company structures in wealth planning.

4. Superannuation Structures

Superannuation is often the most tax-efficient investment environment available in Australia, yet many high-income professionals underutilise it.

Super provides several powerful tax advantages.

Inside super:

- Investment income is taxed at 15%

- Long-term capital gains may be taxed at 10%

- In retirement phase, income and gains may become tax-free

Compared with personal tax rates of up to 47%, the difference can be substantial over time.

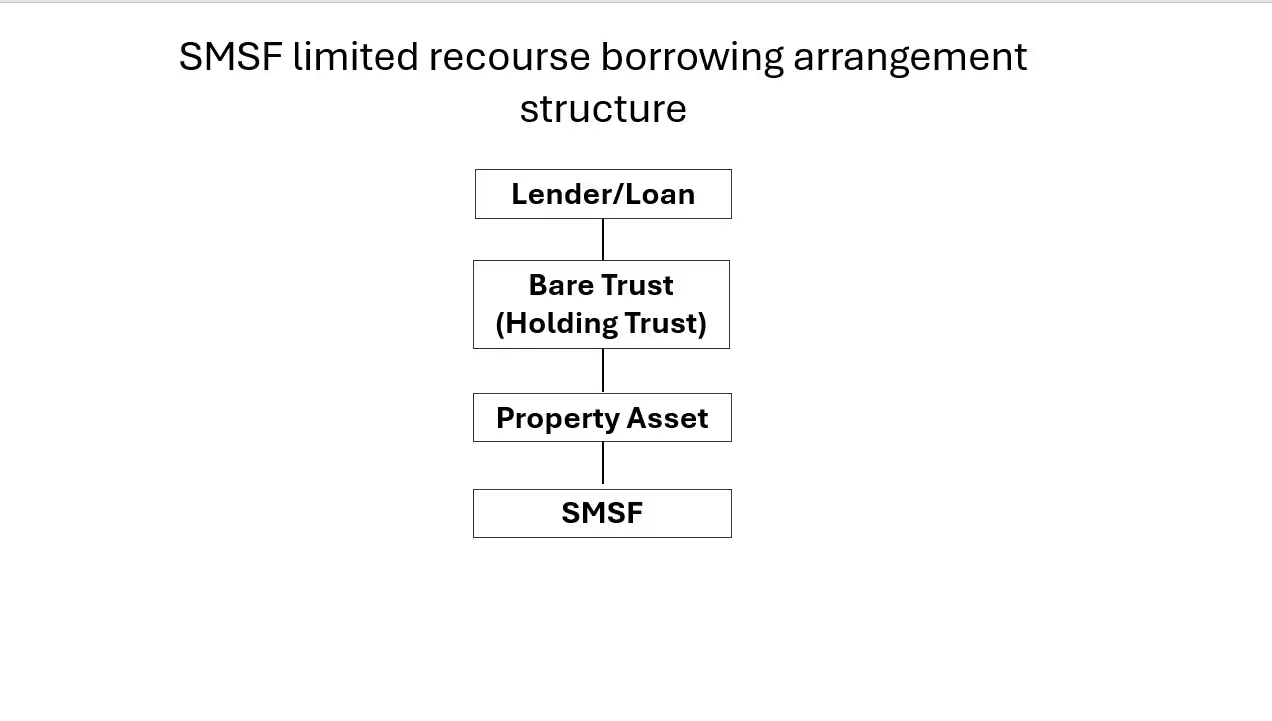

Borrowing Through an SMSF

Some investors use Self-Managed Super Funds (SMSFs) to gain greater investment control.

In certain circumstances, SMSFs can borrow money to invest in property through a structure known as a Limited Recourse Borrowing Arrangement (LRBA).

However, SMSF borrowing is heavily regulated and significantly more complex than traditional property investment.

What Is a Limited Recourse Borrowing Arrangement?

Normally, super funds cannot borrow money.

However, SMSFs can borrow under strict conditions through an LRBA structure.

The key feature of this arrangement is limited recourse.

This means if the loan defaults, the lender’s claim is generally limited only to the specific asset purchased with the loan, not the other assets of the super fund.

How the SMSF Borrowing Structure Works

SMSF borrowing typically involves three components.

The SMSF

The SMSF holds the beneficial ownership of the asset and receives all investment income.

A Bare Trust (Holding Trust)

The asset is legally held in a bare trust until the loan is repaid.

Once the loan is fully repaid, legal ownership transfers to the SMSF.

The Lender

The lender provides the loan under strict LRBA rules.

The loan is secured only against the asset purchased.

Typical SMSF Lending Terms

SMSF lending is generally more conservative than traditional lending.

Typical loan features include:

| Feature | Typical SMSF Loan Terms |

| Loan-to-value ratio | 60% – 70% |

| Interest rates | Higher than standard residential loans |

| Loan terms | Up to 30 years |

| Repayments | Usually principal and interest |

| Liquidity requirements | SMSF must maintain cash reserves |

Because super funds must remain solvent and able to meet obligations, lenders usually require significant liquidity buffers.

Assets an SMSF Can Borrow to Purchase

SMSFs can borrow to acquire a single acquirable asset.

This typically includes:

Residential property

SMSFs can purchase residential investment property, provided:

- It is not used by members or relatives

- It is strictly an investment

Commercial property

Commercial property is often more attractive in SMSFs.

Business owners may purchase their business premises through their super fund, then pay rent to the fund at market rates.

This can create a tax-efficient long-term wealth strategy.

Risks and Limitations of SMSF Borrowing

Despite the benefits, SMSF borrowing also carries risks.

Lower borrowing capacity

SMSF lending is more conservative than personal lending.

Liquidity risks

Super funds must maintain enough liquidity to:

- Pay loan repayments

- Cover expenses

- Meet member benefit payments

Higher costs

SMSF borrowing involves additional costs including:

- Bare trust setup

- Legal documentation

- Specialist lending fees

- Compliance administration

5. Property Ownership Structures

| Structure | Key Benefit | Key Limitation |

|---|---|---|

| Personal | Negative gearing | High tax |

| Trust | Flexibility | Land tax |

| Company | Development use | No CGT discount |

| SMSF | Low tax | Borrowing restrictions |

Property is often the largest investment asset for high-income professionals, which makes the ownership structure extremely important.

Property may be held in:

- Personal names

- Family trusts

- Companies

- Superannuation funds

Each structure has different tax and lending implications.

Tax Environment Comparison Chart

| Structure | Tax Rate |

|---|---|

| Personal | Up to 47% |

| Company | 25–30% |

| Super (Accumulation) | 15% |

| Super (Pension Phase) | 0% |

Personal Ownership for Property

Often preferred when:

- Negative gearing benefits are important

- Capital gains tax discounts are required

- Borrowing capacity needs to be maximised

Trust Ownership for Property

Trusts may be used when:

- Asset protection is important

- Income distribution flexibility is required

- Estate planning flexibility is desired

However, lending and land tax considerations must be assessed.

Company Ownership for Property

Companies are rarely used for long-term property investment because:

- The 50% capital gains tax discount does not apply

- Profits may be taxed twice when distributed

However, companies may still be used in development structures or business-related investments.

Bringing the Structure Together

The most effective wealth strategies rarely rely on just one structure.

Instead, they combine multiple structures depending on the asset type.

A typical framework may look like this:

| Asset Type | Typical Structure |

| Family home | Personal ownership |

| Investment property | Personal or trust |

| Business income | Company |

| Investment income | Family trust |

| Surplus profits | Bucket company |

| Retirement assets | Superannuation |

The key is ensuring these structures work together strategically.

The Role of Professional Advice

Wealth structuring is complex and usually requires a team of advisers, including:

- Financial advisers

- Accountants

- Mortgage brokers

- Lawyers

Each professional helps ensure the strategy is:

- Tax efficient

- Legally compliant

- Compatible with lending policies

- Aligned with long-term financial goals

Final Thoughts

High-income professionals often focus heavily on earning more income.

But the real difference between high income and real wealth often comes down to how that wealth is structured.

The right combination of:

- Personal ownership

- Family trusts

- Companies

- Superannuation

- Strategic property structures

can significantly improve:

- Tax outcomes

- Asset protection

- Borrowing capacity

- Long-term financial flexibility

Structuring wealth correctly is not just about reducing tax today.

It’s about building a framework that allows wealth to grow efficiently for decades.