Most homeowners dream of paying off their mortgage as quickly as possible. Traditional strategies—like budgeting, making extra repayments, or switching to weekly/fortnightly payments—can shave years off your loan term. But while these are helpful, the biggest game-changer comes from leveraging your home equity to invest in another asset, like an investment property.

Minor Strategies That Help

-

Budgeting: Keeping a close eye on income and expenses ensures you can allocate more towards your mortgage.

-

Extra repayments: Any additional payment reduces principal and interest over time, helping your loan term shrink.

-

Weekly or fortnightly payments: By paying more frequently than monthly, you slightly reduce interest accrual, which can save tens of thousands over the life of your loan.

While these strategies are beneficial, they often only trim a few years off your mortgage.

The Major Benefit: Investing

Investing in another asset, such as a rental property, can accelerate your path to being debt-free. Here’s why:

-

Rental income can cover mortgage repayments or even exceed them.

-

Property appreciation builds equity, which can later be used to pay down your home loan.

-

Tax benefits like negative gearing and depreciation may improve your cash flow.

Let’s look at a real-world example.

Example: $800,000 Home Loan

Imagine you have an $800,000 mortgage with a 5% interest rate over 30 years. Instead of only focusing on extra repayments, you decide to invest in a $400,000 investment property with a 20% deposit, financed with a separate mortgage.

-

Home Loan: $800,000, 5% interest, 30 years

-

Investment Property Loan: $320,000 (after 20% deposit)

Investment Strategy

-

Rental income covers a portion of the investment property mortgage.

-

Any surplus cash flow goes towards your home loan.

-

Over 8 years, the investment property appreciates at 7% per year.

After 8 Years

Home Loan:

-

Starting balance: $800,000

-

Additional payments from investment property cash flow: ~$80,000

-

Principal reduction through regular repayments and surplus cash: ~$150,000

Investment Property:

-

Purchase price: $400,000

-

Sale price after 7% annual growth for 8 years: $686,000

-

Selling costs: 2% ($13,720)

-

Capital Gains Tax (assuming 50% discount, 37% tax bracket on gain): ~$44,945

Net proceeds: ~$627,335

By using the proceeds from selling the investment property to pay off the remaining home loan balance, you could clear the $800,000 home loan in just 8 years, rather than 30.

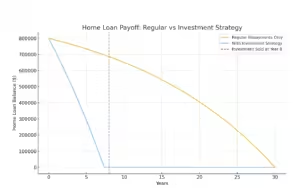

Here’s a visual representation of the strategy:

-

The blue line shows a traditional mortgage with regular repayments only. The loan takes the full 30 years to pay off.

-

The orange line shows the accelerated payoff using the investment property strategy. After 8 years, the investment is sold, and the proceeds drastically reduce the loan balance, clearing it entirely much earlier.

-

The dashed vertical line marks the sale of the investment property at year 8.

This clearly illustrates how leveraging an investment can cut decades off your mortgage timeline.

Why This Works

-

You leverage your equity rather than only relying on savings.

-

Your investment works for you by generating income and growth.

-

You accelerate mortgage payoff without drastically reducing your lifestyle.

Key Takeaway: Minor tweaks like budgeting and extra repayments are helpful, but the fastest way to pay off your home loan is by strategically investing in another asset. By doing so, you not only build wealth but also shorten your journey to financial freedom.